CME: 'Freed-Up' Corn May Still Go To Ethanol

US - Steve Meyer and Len Steiner consider what would happen to the 'freed-up' corn if the RFS waiver passes and goes into effect in the 2011-12 crop year. 11 October 2011

11 October 2011

2 minute read

2 minute read

Several comments or questions on this topic came from DLR readers following our discussion of the proposed Goodlatte-Costa RFS waiver bill. No one knows the answer for sure but our guess is that it will still go into ethanol production.

Ethanol margins are still positive and will likely remain so. Ethanol plants benefit from lower-priced corn just as livestock feeders do. But the fact that that one billion-plus bushels of corn would still go to ethanol does not mean the bill is Quixotic jousting with the ethanol windmills.

It is simply a reflection of economic conditions at the present time. What if the same crop scenario played out with $60/bbl or lower oil? Ethanol margins would be lower the RFS might force relatively high-priced corn into ethanol when ‘true’ economics says it should not go there. That’s the way a ‘free’ market works.

Why has the economic recovery been so slow? We hear that question frequently and read about rather constantly in the press.

We fear that it has become a self-fulfilling prophecy—the slow recovery has caused people to behave in a way that makes for a slow recovery. But there may be much more to it than that.

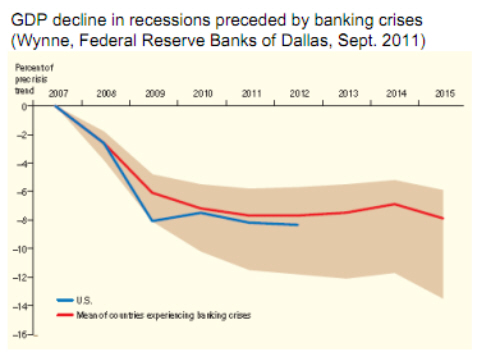

A very interesting (and concise) article in the Federal Reserve Bank of Dallas’s September Economic Letter makes a compelling case that the notable difference between this recession and any other one in the US since World War II is that it was preceded by a banking crisis.

Author Mark A. Wynne goes on to point out that our ‘recovery’ to-date is not that unusual when compared to similar banking crisis-induced recessions in other countries.

The first chart illustrates his findings. It shows the average deviations of output from pre-recessions trend paths in a sample of countries that saw banking crises from the early 1970s to 2002 as well as a 95 per cent confidence interval on those deviations.

There is some disagreement over just when the US crisis began. If one it in 2008 (and many do), the path of US output reductions so far fits the averages of other countries pretty well.

So, while the recovery is an anomaly relative to past US recessions, it is in line with other countries’ recessions that were preceded or begun by banking crises.

Mr Wynne points out that there is not much consensus on why banking difficulties make for more difficult recoveries. He offers that they tend to have more lasting impacts on productivity, employment and investment. Our idea: Perhaps banking-induced recessions rattle consumer confidence and sentiment far more deeply than more normal downward phases of the business cycle.

The entire report can be downloaded [click here].

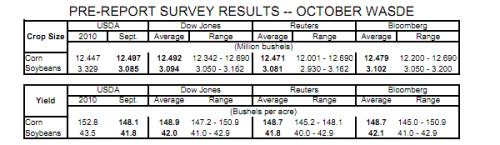

The results of the three major wire services’ surveys of analysts regarding USDA’s September WASDE report, due out today (11 October), appear below.

Analysts expect a slight increase in the corn yield but a slight decrease in the total corn crop. Ditto for soybean yield but they expect, generally, a slightly larger soybean crop.

They also expect 2012 corn carry-out stocks of about 800 million bushels, up sharply from USDA’s August estimate of 672 million bushels.

Further Reading

| - | You can view the full report by clicking here. |