CME: Export Data 'More of the Same'

US - Rather lost amid the flurry of talk regarding corn and soybean yields, crop sizes, carry-out stocks, etc. was the release on Thursday (9 August) of export data for June and it generally indicated “more of the same” for beef, pork and chicken. 15 August 2012

15 August 2012

4 minute read

4 minute read

By:

By: Some highlights of

last week’s report are:

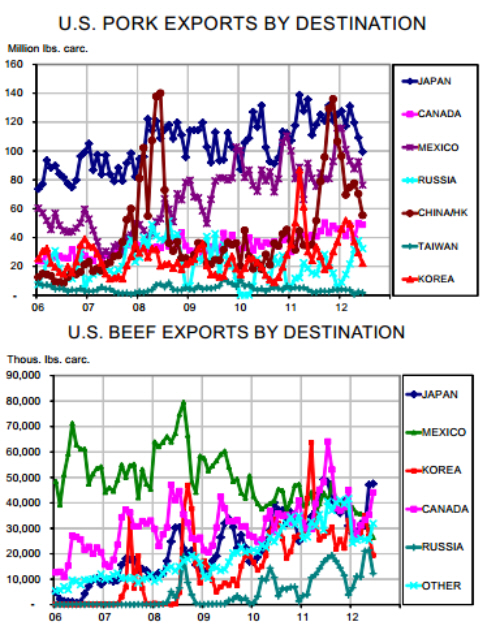

Shipments of pork declined for every major market in June from

their May levels but remained, in total, 7.8% larger than last year

using carcass weight equivalent (CWE) data. The top chart at

right shows these data for the top seven U.S. pork destinations.

June exports to China/HK (55.4 million pounds) were sharply lower than the Feb-May average of just over 70 million pounds but

the June total was still 57.6% higher than one year ago. Japan

and Mexico remain the two largest destinations for U.S. pork.

U.S pork exports to Korea continued to decline in June and were

7.8% lower than those of June 2011. Those June 2011 shipments were still being influenced by Koreas foot and mouth disease losses, however, so the year-on-year decline is no surprise.

June 2012 shipments were 12% larger than those of June 2010

when Korea’s domestic supply was at pre-FMD levels.

Pork exports remained 12% higher, year-to-date, than in 2011.

The 2.746 billion pounds of CWE product exported this year represents 24.1% of U.S. commercial pork production (11.377 billion

pounds) through June. That percentage, should it hold for the

remainder of 2012, would be record high.

The value of U.S. pork exports in June ($409.562 million) was

4.3% higher than last year and brings the YTD total to $2.758

billion, 12.1% higher than in 2011.

Pork variety meat (PVM) exports were down sharply from both

last month (-19.4%) and last June (-24.1%) but the value of June

PVM exports was still 4.1% higher than last year. YTD PVM

exports are 15% lower than in 2011 through June but the value of

those exports is UP 24.8% — a remarkable figure, implying

MUCH better unit pricing so far in 2012.

For only the fourth time since BSE stopped U.S. beef exports in

early 2004, Japan was the largest destination of U.S. beef shipments in June, taking 47.494 million pounds, CWE. June is the

first time since 2003 that Japan has been the largest destination

in successive months even though this year’s June business was

3.4% smaller than last year’s.

Total beef exports continue lag those of 2011 substantially with

the 2012 total of 1.183 billion pounds, CWE, falling 11.4% short of

2011. The value of June beef exports, however, was slightly larger (0.9%) than one year ago. That brings YTD beef export value

to $2.315 billion, 3.7% higher than at the same time last year.

Exports of beef to Mexico continued to struggle in June. The

month’s 26.4 million pounds, CWE, was nearly 40% lower than

one year ago and brings the YTD figure to only $200.2 million,

17% less than in 2011.

Other significant drags on June beef exports were Russia (-27.2%

yr/yr) and Korea (27.5% yr/yr). Exports to Canada were sharply

higher than in May but remained 8.6% lower than last year.

YTD chicken exports continued to exceed year-ago levels by just

over 13% with June shipments of 593.3 million pounds being

12.3% higher than those of June 2011.

Mexico remains the largest destination for U.S. chicken with 103.6

million pounds heading south in June. That total is 15% larger

than last year and brings shipments to Mexico to +17.7%, YTD.

Shipments to Russia, the Baltics and former CIS countries are up

164%, 146% and 106% YTD through June.

Some lesser known markets have become VERY important to the

U.S. chicken industry. They, with their June rank, include Angola

(5), Cuba (6), Kazakhstan (7), Lithuania (8), Taiwan (10), Ukraine

(11), Iraq (12), United Arab Emirates (13), Haiti (14) and Phillipines (15). All are larger markets for U.S. chicken than are

Korea, China (without Hong Kong) or Japan.