Peoples' Republic of China - Poultry and Products Semi Annual Report 2008

By the USDA, Foreign Agricultural Service - This article provides the poultry industry data from the USDA FAS Poultry and Products Semi-Annual 2008 report for the Peoples' Republic of China. A link to the full report is also provided. The full report includes all the tabular data which we have ommited from this article. 14 March 2008

14 March 2008

11 minute read

11 minute read

Executive Summary

FAS Beijing forecasts China’s broiler production in 2008 to increase by nine percent to 12.5 MMT because of strong local demand. Interest in broiler meat is expected to stay high because of a continuing pork shortage and resulting high prices. The expected slow recovery in the swine sector will likely keep prices high, encouraging the consumption of broiler meat as consumers substitute poultry meat for pork.

Strong demand, high prices, and the strong Renminbi are also expected to push China’s 2008 boiler meat imports up by 24 percent to 600,000 MT. Poultry meat imports are also expanding beyond broilers. In 2007, China imported increasing volumes of turkey meat, a non-traditional product. Imports rose dramatically from 12,191 MT in 2005 to 29,808 MT, a 145 percent increase. Industry sources believe this change was the result of larger numbers of foreigners living in China and the increasing influence of western cuisine among the younger Chinese.

China’s 2008 broiler exports are forecast to increase by 12 percent to 400,000 MT because of increased demand in export markets. Around 90 percent of exports go to Japan, Hong Kong, and South Korea.

China’s ban on imports of poultry products from seven U.S. states with past Low Pathogenic Avian Influenza (LPAI) outbreaks may not be lifted in 2008 (Please see CH7077 for detailed information). Resolution of LPAI and other important trade issues has been linked with market access for exports of China’s cooked poultry to the United States.

Note: No data included in this report is official. All official USDA data is available at

http://www.fas.usda.gov/psdonlineonline.

Production

Broiler Production Keeps Rising

FAS Beijing forecasts broiler meat production in 2008 to increase by nine percent to 12.5 MMT. This change came on the heels of a 12 percent increase in 2007 to an estimated 11.5 MMT. This sharp increase came because of a sharp decline in pork production caused by swine blue ear disease. The disease struck during the second half of 2006 and the first half of 2007, causing a considerable shortfall in overall meat supplies. As the second most preferred animal protein in China, broiler meat is an important substitute when pork prices are high. Post expects broiler meat to continue as the main substitute for pork in 2008 since swine production is only expected to recover slowly.

The growth rate in China’s broiler meat production is expected to be below 2007’s feverish pace because broiler farms were hard hit by the worst snowstorms in the last 50 years. According to the Ministry of Agriculture (MOA), at the end of January and beginning of February 2008, 25 provinces in China were hit by the snowstorms that caused 129 human deaths and resulted in economic losses totaling RMB 151.7 billion ($21.4 billion). On February 19, MOA reported in its Work Plan to Resume and Develop Livestock Production After Disasters that as of February 14, the snow storms killed 63.1 million birds and interfered with operations in major broiler producing provinces such as Guangdong, Henan, and Jiangsu.

The increase in broiler production will also likely be slowed by higher production costs. High commodity prices have had an important effect in addition to rising prices for water, electricity, energy, transportation, and increasing workers’ salaries. Other escalating costs include animal disease control and environmental protection.

While labor was not traditionally an important cost in China’s rural areas, this is no longer true because mass migration is shrinking the labor pool. According to the second national agriculture census published by the National Statistics Bureau (NSB) on February 21, 2008, more than 131.8 million rural laborers moved to urban areas by the end of the 2006 -- with male labor accounting for 64 percent of the total. In addition, China’s new Labor Contract Law became effective on January 1, 2008. This law may attract even more rural labors to urban areas because it mandates a package of benefits and salaries that farms have difficulty matching. The law also requires employers to provide proper benefits and salaries, which will increase production costs further. Even for those who stay on the farm, paid work in the village is more attractive than farming. In some regions, more than half of rural income now comes from off-farm sources. The coming labor shortage could become an important bottleneck in the development of the poultry sector.

On January 18, 2008, the National Statistics Bureau announced that China’s PPI in January was up 7.1 percent compared with a year ago. This was the largest monthly rise in three years. Prices increased for water, electricity, transportation, energy, and labor because of inflation. High production costs combined with the strong Renminbi could make Chinese broiler products less competitive in the international market in the next couple of years while encouraging large imports. On the other hand, a strong Renminbi should work against inflation by making imports less expensive for Chinese consumers.

Another uncertainty is the possibility of future outbreaks of highly pathogenic avian influenza (HPAI). From January to February 2008, there were three outbreaks of human infection with HPAI and all of them died. Also, there were three outbreaks of HPAI on poultry farms, two in Tibet (culled 13,000 and 7,600 birds respectively), and one in Guizhou Province (culled 230,000 birds). The HPAI situation will continue to be a wild card in both the production and consumption of all poultry meat.

20-Year Production Trends

Total poultry meat production has risen more than ten-fold over the last 20 years. In 1986 it totaled 1.49 MMT while in 2006 it was 15.1 MMT. Although pork still remains China’s most widely consumed meat, poultry production has benefitted from lower costs compared to swine, a faster reproduction cycle, and earlier modernization that reduced the number of backyard farms. Some of the most modern facilities are very large. For example, the Xinchang Company in Shandong is building a new processing plant with a daily slaughter capacity at 300,000 birds, which will be 50 percent of Tyson’s slaughter in the United States. FAS Beijing expects that the poultry sector will continue to be the most modern and capital intensive meat sector in China.

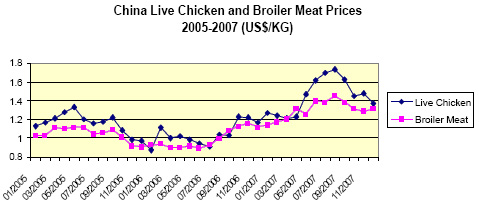

Broilers Stay Cheaper than Pork

China’s average year-on-year wholesale broiler price in 2007 climbed 31 percent to US$1.30 per kilogram while the live chicken price went up by 39 percent to $1.45 per kilogram. At the same time, the average year-on-year pork price in 2007 raced up 56 percent to $2.21 per kilogram because of short supplies. Broiler prices have stayed below pork prices because of a large increase in broiler production resulting from reduced HPAI outbreaks in 2007. At the same time, relatively stable feed corn supplies have kept broiler prices lower, although broiler prices have increased because of inflation and extra demand caused by substitution from pork. FAS Beijing forecasts that China’s 2008 broiler prices will likely remain high but stable during the first half of 2008 with a slight easing possible as pork supplies slowly improve in the latter half of the year.

With more than 130 million mostly poor urban migrants who spend almost half their income on food, the Chinese Government is concerned that escalating meat prices will lead to instability. In response to higher meat prices, the National Development and Reform Commission (NDRC), China’s top economic planner, announced in mid January 2008 to mandatory price caps on a range of products, including grain, edible oils, meat, milk, and eggs. Food producers have to apply for verification and approval by the government for any new price hikes. At the same time, China is expected to put more imported meat from strategic reserves on the market to curb meat prices and support consumption.

Consumption

20-Year Consumption Trends

Increased incomes have increased meat consumption and changed the market shares for different meats. Over the last couple decades, pork has slowly lost market share to other meats. For example, pork accounted for 85 percent of meat consumption in 1986, while making up only 65 percent in 2006. Broiler meat accounted for eight percent in 1986, but increased to 13 percent in 2006. Per capita poultry consumption was 1.13 kilograms in 1984, and it was 11.2 kilograms in 2006. Per capita broiler meat stands at 8 kilograms per capita. As a result, poultry meat is the second largest meat protein source after pork. The local industry believes that in the last ten years, poultry consumption increased 20 percent year-on-year because of the development of fast food restaurants in China such as KFC and McDonalds. In the years to come, demand for different kinds of meat will likely move back and forth depending on prices or outbreaks of animal diseases.

FAS Beijing forecasts China’s broiler consumption in 2008 to increase by eight percent to 12.7 MMT because of increased domestic production and large imports. Since Chinese consumers are price-sensitive, many of them turned to poultry meat when pork prices were high. In order to support meat consumption, the government imposes prices caps on major food products while providing poor consumers with RMB 20-30 ($2.9 - 4.3) per month per person to buy meat for about six months. Live chickens sold on the markets of agricultural produce to individual families are normally local breed yellow-feathered chicken (for all kinds of menus), black chicken (for soup), or spent hens (for soup). Native brand“San Huang” chicken prices are higher than Western chicken breeds because buyers believe that have a more fragrant smell and taste compared with western breed broilers that are mainly sold to restaurants, lunch box companies, cafeterias at schools, organizations, and the military.

Outside volume increases, there is another significant change in meat consumption caused by people moving off the farm. In the past, thousands of family households had backyard hogs for self sufficiency. After many backyard operations closed because of blue ear disease and other problems , those farmers who formerly consumed their own products now need to buy meat on the market. This means more meat will be traded formally as opposed to the past practice of on-farm consumption or small-scale cash sales in a nearby village.

Trade

Record Imports, Sanitary Problems Remain

FAS Beijing forecasts China’s broiler meat imports in 2008 to increase by 24 percent to 600,000 MT from the previous year’s 482,000 MT (ready-to-cook weight). Chicken paw imports are expected to increase by one-third to 723,600 MT from the previous years’ 544,088 MT. These totals include both direct shipments and Hong Kong re-exports to the mainland.

China’s broiler imports are the largest source of imported meat. China’s total imports (broiler meat and chicken paws) in 2007 from the world were valued at nearly $926.2 million while imports from the United States were valued at nearly $558.6 million. These strong imports are not likely to fall. Chicken paw imports account for nearly 50 percent of China’s total broiler imports. The short domestic meat supply and strong Chinese interest in eating chicken paws will likely continue drive imports up in 2008.

China bans imports from seven U.S. States because of low pathogenic avian influenza (LPAI) reported in FAS Beijing’s last annual poultry report CH7077. Although China’s ban may be contrary to OIE standards, negotiations continue. Resolution of this issue and other important SPS trade issues has been linked with market access for exports of China’s cooked poultry exports to the United States – an issue that remains unresolved. Although FAS Beijing does not expect major trade disruptions in the short-term, failure to resolve outstanding sanitary issues probably means that U.S. exports will continue to face problems at the border.

Rising Turkey Meat Imports, A Non-Traditional Product

In 2007, China’s turkey imports, a non-traditional meat product, increased from 12,191 MT valued at $10.2 million in 2005 to 29,808 MT valued at $27.9 million. Turkey products are mainly consumed by foreigners resident in China or tourists. At the same time, supermarkets in large cities start have started selling cooked turkey parts, such as wings or legs, for Chinese consumers. Unlike the United States, the Chinese do not buy whole birds since they do not like breast meat. Those Chinese who lived abroad before are part of the consumers are also part of this trend. The rising consumption among younger generation is also influenced by the western traditions, such as the Thanksgiving. Since China’s turkey production is almost nil, China also imports turkey meat to satisfy consumer demand.

Rising Exports

FAS Beijing forecasts China’s broiler meat exports in 2008 to increase by 12 percent to 400,000 MT. Japan is expected to continue be China’s top export market followed by Hong Kong and South Korea, with all three countries accounting for 90 percent of China’s total exports. Cooked products will remain the backbone products as last year. To protect China’s poultry export interests, both AQSIQ (in [2007] No. 212 document) and MOA have imposed strict requirements for poultry raising, processing, and management for exported products. One of the major reasons why China has been especially strict with exports is its interest in securing export markets overseas. This not only can bring increased revenue for Chinese firms, but also sends the message to Chinese consumers that the product they buy from local firms is safe.

Poultry Eggs Stable

FAS Beijing (Post) forecasts China’s total poultry egg production in 2008 to increase by two percent to 31.1 MT from estimated 30.3 MT in 2007. Most eggs consumed are fresh-shelled table eggs. Only a very small volume of eggs is processed or preserved. China’s imports of fresh eggs are nil. Its exports are mainly to Hong Kong and Macau.

Further Reading

|

|

- You can view the full report, including tables, by clicking here. |

List of Articles in this series

To view our complete list of Poultry and Products Annual and Semi Annual reports, please click hereMarch 2008