CME: <i>Cold Storage</i> Report Supportive Of Meat Prices

US - USDA released on Thursday afternoon its latest Cold Storage report, offering a snapshot of the supply of beef, pork and poultry in cold storage as of 31 August 2011. The results of the survey were generally supportive for meat prices going forward, particularly for pork and chicken, write Steve Meyer and Len Steiner. 26 September 2011

26 September 2011

4 minute read

4 minute read

The impact on futures will likely be limited, however, as market participants are

more focused on what is happening in outside markets.

Commodity and equity markets declined sharply on Thursday but

have bounced back in overnight trading.

Concerns about the

global economic outlook and the risk of a sovereign debt crisis in

Europe will likely continue to have an outsize impact on markets, eclipsing, at least in the short term, fundamentals. Below

are some of the highlights from the latest cold storage report.

You can find full details on page four (see full report).

Beef: Total beef stocks on 31 August were 429.2 million pounds, 10.8 per cent higher than the same period a year ago but

still some three per cent lower than the five year average.

Beef inventories rose 3.4 per cent compared to the previous month, in line with

historical averages. Seasonally beef inventories increase going

into the fall and current stocks are far from burdensome.

Beef

inventories should continue to increase into Q4 as retailers and

foodservice operators build stocks ahead of year end holidays.

Pork: Total pork inventories at the end of August

were reported at 440.7 million pounds, 13.5 per cent higher than a

year ago but four per cent lower than the five year average.

In the last

five years pork stocks on average have declined about one per cent from

July to August. This August, however, pork inventories declined three per cent, an indication that domestic and export demand remains in good shape.

Total pork inventories are higher than

last year but this largely reflects the need for larger staging

stocks given the mammoth increase in export business. Some of

our work in this area shows a strong relationship between export volume and the level of inventories required to service this

business.

Ham stocks at the end of August were 148.8 million

pounds, 4.7 per cent higher than a year ago and 7.6 per cent higher than the

five year average.

Inventory build for the month was in line

with historical trends. Belly inventories seasonally decline into

September and this year is no different.

Belly stocks at the end

of August were down 48.7 per cent from the previous month compared

to a normal drawdown pace of about 45 per cent.

Inventories of pork

loins at the end of August were 22.5 million pounds, 46 per cent higher

than a year ago but we suspect this was in part driven by improvement in export business. Pork loin prices in the domestic

market remain very strong.

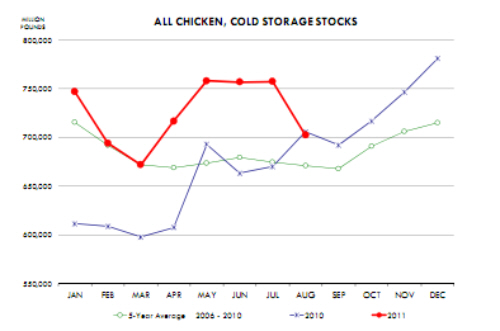

Broilers: One of the more positive signs in the report

was the sharp drawdown in chicken inventories during

August.

Broiler stocks in August were 702.2 million pounds,

7.2 per cent lower than just a month ago. Total broiler inventories are

now slightly lower than the previous year but still 4.7 per cent higher

than a year ago.

Cutbacks in production appear to be having an

effect. Inventories of leg quarters, an export item, were down

21.4 per cent from the previous month and are now 23.5 per cent lower than

the previous year.

Inventories of breast meat remain heavy and

it will take another two to three months to bring them in balance.

Further Reading

| - | You can view the full report by clicking here. |