CME: Broiler Margins See Slight Improvement

US - Broiler margins improved a bit last week but companies are still losing money on each pound sold, write Steve Meyer and Len Steiner. 3 October 2011

3 October 2011

4 minute read

4 minute read

So much for a 'slightly bearish' Hogs and Pigs Report as CME Group Lean Hogs futures rallied on Thursday (29 September). Market observers attributed the rally to higher cash hogs (and Ia-Minn negotiated hogs were up over $1.50/cwt), higher cutout values and rumours of more orders from China.

Those were no doubt at play and it is important to note that the primary bullish action was in the nearby contracts that would not be impacted by the most bearish features of the report, farrowing intentions and continued litter size growth.

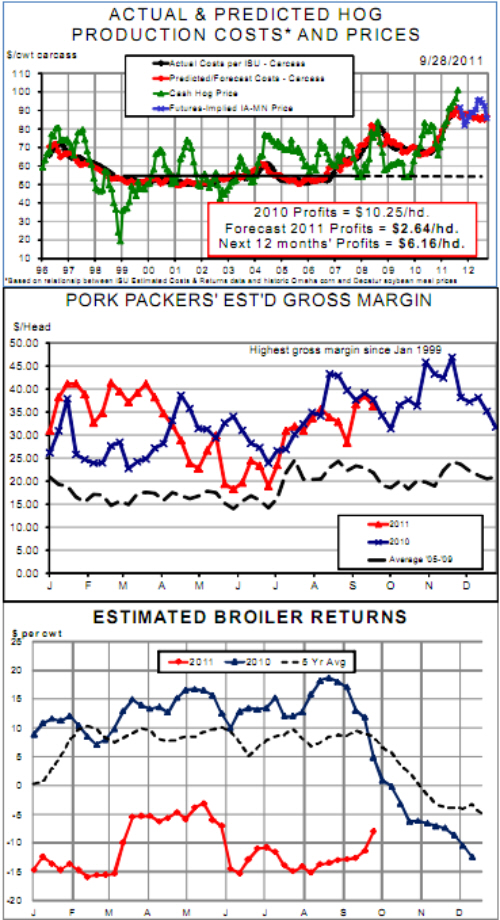

The rally was a pleasant surprise for producers, pushing December futures above $85 — a level pegged as a pricing target by a number of analysts.

Yesterday’s rally pushed profit potential for pork producers above $6 per head over the next 12 months. As can be seen in the chart below, in spite of record-high costs of production, producers have enjoyed a profitable summer.

Iowa State University returns estimates indicated profits of $11 to $15 per head from May through July and a surprising $21.31 per head in August when live hog prices hit record highs.

Current corn, soybean meal and lean hogs futures indicate profits of about $10//head for September and relatively small losses for October through January.

At present, markets indicate a return to profits in February and a relatively normal seasonal profit pattern through September 2012.

Now the question becomes “With more certainty regarding the level of feed ingredient production and prices, will these profit prospects be large enough to drive further expansion?”

We know that Cargill will continue populating the former Premium Standard/ Smithfield operations in West Texas. Effective risk management on the part of a number of major players has left them with the financial resources to grow in coming months but will they opt to invest in more gestation and farrowing facilities? We think the reaction will be limited primarily due to continue feed cost risks. Now we can all start worrying about the 2012 crop.

Pork packer margins have improved steadily since June. That is no surprise since margins almost always reach their seasonal highs in the fourth quarter when strong consumer demand keeps pork prices strong relative to the hog prices that packers must pay to get sufficient supplies.

As always, we point out that the numbers in the chart at right are gross margins — simply the value of the carcass plus the value of the by-products less the cost of the hogs. But as can be seen, these levels in the mid-$30s are very good and have persisted for most of the past two years.

When will someone build more capacity to take advantage of these margins? That’s a good question since existing players may not see expansion as good for their current businesses and we know of no “new players.”

Finally, broiler margins improved a bit last week but it only means that companies are losing less than 10 cents/pound for the first time since late May.

The huge cuts in egg sets (-8.6 and –7.4 per cent the past two weeks) and placements (-5.7 and -4.6 per cent the past two weeks) continue the pattern of larger responses to these losses but have not stopped the bleeding yet.