CME: No Change Expected in Grain Supply

US - On Friday (9 December), USDA will publish its monthly update of crop and livestock projections for the remainder of 2011 and 2012. As usual, grain data will be closely watched although not much change is expected from a supply perspective, write Steve Meyer and Len Steiner. 8 December 2011

8 December 2011

2 minute read

2 minute read

By:

By: USDA will wait for the results of the quarterly stocks survey and any revisions in the production data will not be available until January. We could see some revisions, however, in the demand numbers, particularly export projections.

The November update kept export numbers unchanged at 1.6 billion bushels, 13 per cent lower than a year ago and 19% lower than two years ago. Extremely high corn prices likely have rationed out some export demand.

In addition, reports are pouring in of higher feed wheat availability in global markets. These reports point out that feed wheat from a number of key areas, such as the Black Sea region and Australia, are now competitively priced vs. US corn.

As a result, market participants will be paying close attention to USDA revisions in global supply data. For instance, Australia recently increased its wheat supply forecasts to a little over 28,000 MT, eight per cent over the November USDA projections.

Much of this increase in output will likely go into feed supplies as Australian reports indicate ample moisture during winter and spring (southern hemisphere). There have also been reports that China expects another bumper corn harvest. Trade has learned to be very cautious about Chinese data as official reports often belie what markets reveal via pricing.

Regardless, USDA will make its best attempt at gauging Chinese supplies and official reports are part of the mosaic.

A survey of analysts conducted by Dow Jones indicated that on average they expect US domestic corn ending stocks for the 2011/12 marketing year at 831 million bushels, about unchanged compared to the November USDA estimate.

It appears that analysts expect any reductions in exports to be offset by higher domestic use numbers, either for industrial use (ethanol) or feed use.

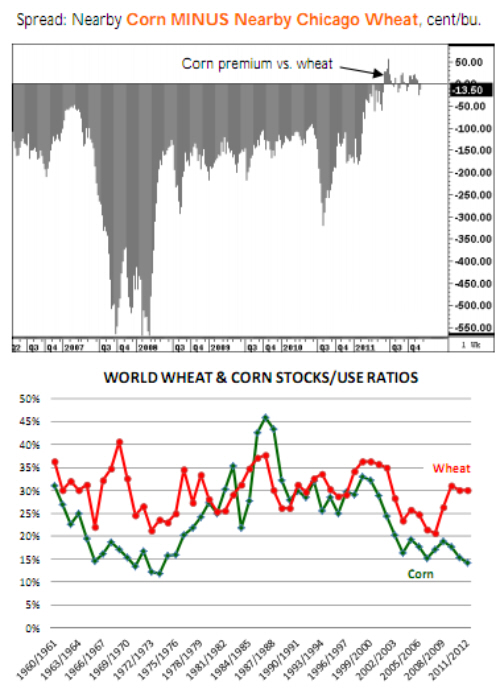

The relationship between wheat and corn prices has shifted in recent months as corn supplies have become increasingly tighter relative to wheat. The top chart shows that for a number of months this year, nearby corn futures have traded at a premium to soft red winter wheat (Chicago).

High protein wheat (MN) continues to maintain significant premiums which is to be expected given limited supplies in the US and Canadian markets. The bottom chart shows what is happening on a global scale with corn and wheat.

While the corn stocks to use ratio is currently nearing a forty year low, wheat stocks have recovered and are near long term trends. The upcoming USDA report could widen the gap further as high prices and better weather boost wheat supplies in main production areas.