CME: Job Growth Has Returned

US - Friday’s employment reports from the Bureau of Labour Statistics indicate that job growth has returned, write Steve Meyer and Len Steiner. 6 February 2012

6 February 2012

3 minute read

3 minute read

By:

By: We believe the

January numbers will be supportive to meat and poultry demand.

Some of the key numbers from the reports are:

The unemployment rate fell to 8.3%, its lowest level since February 2009. That number compares to 8.5% last month and 9.1%

one year ago. The kicker on this improvement, though, is that

the rate of long-term (over 27 weeks) unemployment remains at

3.6%.

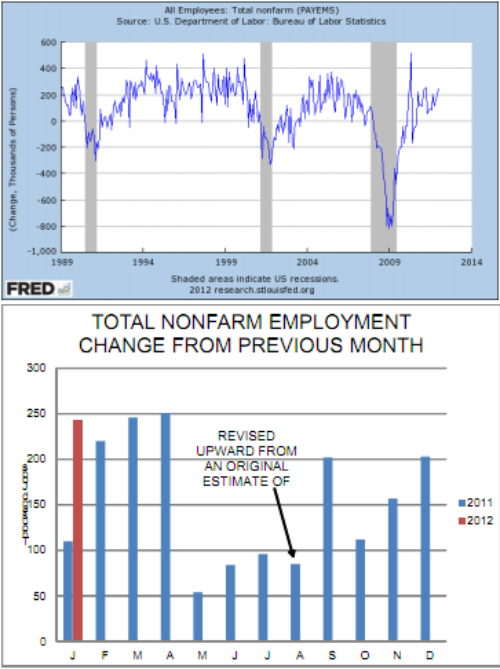

Total nonfarm employment rose to 132.409 million people in January, a gain of 243,000 jobs from the revised December level and

1.953 million since January 2011. The chart at right shows these

data back to January 1989 and comes directly from the Federal

Reserve Economic Data (FRED) system at the Federal Reserve

Bank of St. Louis (http://research.stlouisfed.org/fred2/). We like

their charts because they include the shaded areas that mark

recessions as called by the Bureau of Economic Analysis. Dr.

Robert Dieli of RDLB, Inc. and www.nospinforecast.com makes

three very useful observations of this chart in his Employment

Situation report that was released Friday afternoon. First, he

points out that BEA sets the onset of recessions where this line

crosses zero. Second, BEA looks for persistent and widespread

DECLINES in total employment. Finally, he states “I don’t see

those right now. Do you?” Our answer is “No”.

January’s employment level is back to the level of December

2004. As Dr. Dieli points out, this date keeps sliding forward with

every improvement in employment, gaining 3 months in January.

When employment was at its lowest level for the past recession

back in February 2010, this “worst since” date was August 1999.

A boat load of revisions pushed the employment numbers for all

of 2011 higher. They included 5 months in which BLS added

over 200,000 jobs to the previously reported numbers. Perhaps

the most important of these was a much smaller change to the

August 2011 numbers. The first estimate for that month showed

NO growth in employment and set off a wave of concern that the

economy was slipping back into recession. The January revision

for August shows a gain of 85,000 jobs for the month — nothing

to write home about but a number that would not likely have set

of “The sky is falling!” cries from many economists.

Private sector payrolls continued to lead the way on employment

growth, gaining 257,000 in January. Comparing that number to

total gains points out that government payrolls continued to

shrink, primarily the victims of lower revenues and cuts at state

and local levels.

Our discussion of relative beef cut prices on Friday engendered a lively e-mail discussion with some readers. We

thought some were certainly noteworthy.

Several readers pointed out he influence of exports on the

values of the round and chuck (ie. “end meat” ) cuts. U.S. beef exports were once dominated by shipments to Japan, a market that generally demands higher-quality product and whose import policies require higher valued product. The growing importance of a number of

more price-conscious markets (e.g. Mexico, South Korea, VietnamChina) have placed more importance on lower value cuts.

As for brisket, Jim Robb of the LMIC in Denver points out —

“Barbecue is now EVERYWHERE!” He is correct and that factor is a

contributor on the pork side as well. It seems that pulled pork sandwiches, once the territory of “barbecue joints” only, are available in

about any kind or level of restaurant these days and that popularity—

along with exports — have pushed butt prices higher relative to other

pork cuts. Robb also pointed out that many of the value-added beef

cuts developed over the pat few years have come from the chuck.

Finally, there is the issue of cut size. Is our seeming inability

to cut a rib eye or loin eye muscle in two or more parts reducing the

unit value of beef and pork middle meats? Those steaks and chops

are now HUGE and larger than most people can eat at one sitting.

Further Reading

| - | You can view the full report by clicking here. |