CME: CME Host WASDE Online Discussion

US - CME Group will host an interactive online discussion session at 2:30 p.m. tomorrow (Tuesday 10 July) regarding Wednesday’s USDA Crop Production and World Agricultural Supply and Demand (WASDE) reports. 9 July 2012

9 July 2012

3 minute read

3 minute read

By:

By:

The speakers for the event will be Dan Basse,

President of AgResource Company and Terry Roggensack, CoOwner of The Hightower Report. Click here to register for the

online discussion.

Steve Meyer writes: The result of some windshield crop

survey time over the past two weeks confirms the dire situation in

southern Indiana and Illinois. Corn in those areas looks very bad.

Some acres will not be salvaged. Others will see very low yields.

Central Iowa and Illinois from the Quad Cities to Champaign

LOOKED pretty good but was virtually all tasseled with much of it in

the pollination stage during last week’s extreme heat. The Springfield area was, generally, in the same boat two weeks ago. Everywhere I travelled was in dire need of rain. Grasses in pastures and

roadsides were brown everywhere. The soybeans still looked pretty good. I’m sure some plants were smaller than desired but there

was little “from the road” damage. Some timely rains would very

likely still result in decent yields from most acres but those showers

had better arrive soon. Today’s Crop Progress report will likely

show 40% or so of soybean acres blooming. Last week’s figure

was 26%, more than double the 5-year average of 12%. One thing

appears certain — The early-planted corn crop did not “miss the

heat” with early pollination.

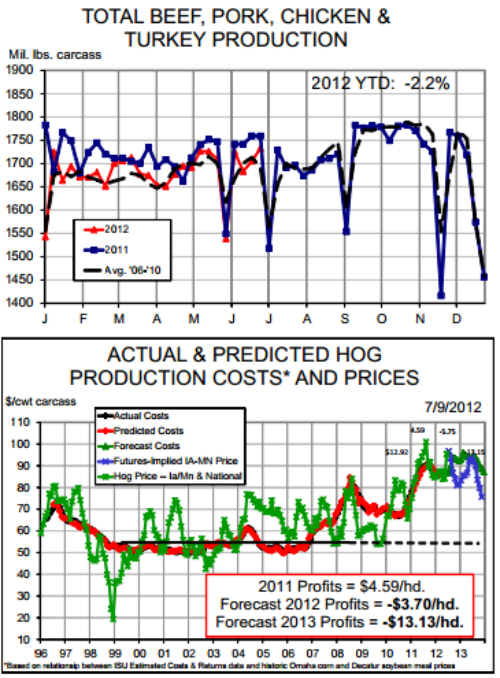

Last week’s total meat and poultry output of 1.612

billion pounds was 2.3% lower than one year ago and brought

the year-to-date total, based on daily data, to 44.525 billion

pounds, 1.8% lower than in 2011. The chart at right shows weekly data for total meat and poultry output. Note that it doe s not include data for last week and that the year-on-year comparison for

these weekly data stands at –2.2%. It is clear to see that the yearon-year declines became much larger in June, driven primarily by

sharply lower poultry output and pork production much closer to

year-ago levels than was seen in April and May.

We still expect the year-on-year comparisons for chicken

to get more and more positive as this year’s weekly data are compared to the sharply lower level’s witnessed last year after the industry’s downsizing got rolling in earnest. Broiler egg sets for two

weeks ago (the most recent data available) of 196.2 million were

only 0.5% lower than in 2011. Chick placements that week numbered 165.7 million, just 1.8% lower than last year.

Our expectations for beef are just the opposite. Fed cattle

supplies will continue to run below year-ago levels and we think the

large positive impact of this year’s carcass weights will get smaller

primarily due to higher feed costs. One contributing factor is that

distillers grains with solubles (DGS) do not help costs as much as

they once did. The price of DDGS (the dried version of DGS) had

been, until just last week, above 90% of the price of corn on perpound basis since late March. It dropped to 87% last week but we

expect it to go higher as ethanol production drops in response to

lower corn prices. DDGS will still be a major component of cattle

diets since DDGS-corn price ratios at this level are even more disadvantageous to pork and poultry producers. But they will provide

little cost relief to cattle feeders, putting some pressure on weights

— at least on a year-on-year basis.

Hot weather has already begun to impact pork supplies

and high feed costs will play a role as well for the remainder of the

year. Last week’s producer-sold barrows and gilts reported to the

mandatory price reporting system averaged 201.9 pounds, 0.6

pounds or 0.3% lower than last year. That is the first time since

February — and only the second time this year — that weights

were lower than in 2011. Looking forward, average production

costs are now forecast to go above $94/cwt for hogs sold in September and to AVERAGE more than $93/cwt for all of 2013. Costs

that high will impact market weights for the foreseeable future.