CME: Grain Markets Very Volatile

US - Grain markets have been particularly volatile in recent weeks as market participants try to assess the price levels required to ration available grain supplies for 2012/13 marketing year, write Steve Meyer and Len Steiner. 17 September 2012

17 September 2012

2 minute read

2 minute read

By:

By:

Corn futures were higher on Friday, buoyed by

optimism that another round of bond buying by the Federal Reserve could stoke inflation, especially inflation in commodity markets.

It appears that the optimism was short lived, however, as

markets turned negative over the weekend and they are currently

trading as much as 15 cents lower corn and 37 cents lower soybeans.

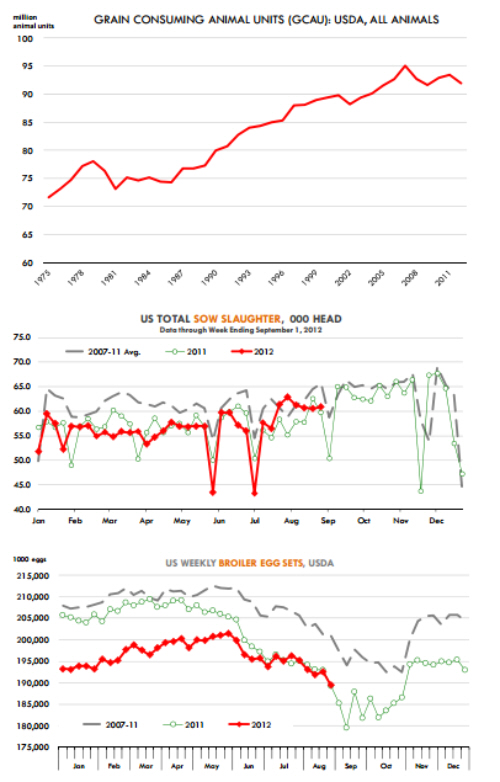

It is interesting to note that USDA currently expects only a

very modest reduction in the number of grain consuming animal

units (GCAU). For those unfamiliar with this index, it purports to

convert all livestock and poultry into a consistent unit. The most

recent data shows that for the current marketing year, USDA projects 91.944 million units, down 1.6% from the previous year but

slightly higher than what they were in 2009.

Corn production for

2012/13, on the other hand, is currently projected to be down 13.2%

from last year while ethanol production (and DDG production as a

result) is expected to be down 10% from a year ago.

Different from

last year, when wheat, meal and other feed supplies were somewhat more abundant, market participants now have to consider the

impact of short supplies across multiple commodities.

Soybean

meal production for 2012-13 is currently projected to be down 13%

from last year and hay production is forecast to be down 20% for

alfalfa and down 12% for all other hays. Sharp reductions in feed

availability imply a dramatic reduction in the amount of feed available for GCAU and will likely force further liquidation in a number

of sectors. At this point, it is a matter of how high prices need to be

in order to reduce feeding. Sow slaughter so far continues to track

close to year ago levels (see chart). Similarly, broiler egg sets are

almost identical to what they were last year. The conventional view

is that broiler producers will be the first to cut back numbers as it

is theoretically easier to do so with poultry rather than livestock.

However, it is unclear how easy this will be for the broiler industry

given the significant vertical integration and the end user contracts

that producers have on the books. In recent years the poultry industry has sought to price some of their product off the grain market. As a result, the slowdown in production will depend on how

quickly end users are able/willing to reduce demand. Cow-calf producers have yet to cull beef cow herds, largely because the situation

in the Southern Plains is better than what it was last year. Cow

slaughter currently down 5% from last year, with beef cow slaughter down 20% from last year while dairy cow slaughter up 17%