Positive Outlook for Global Meat Market

GLOBAL - The outlook for the global meat market is largely positive, according to a joint Agricultural Outlook report from the OECD and FAO. 27 August 2015

27 August 2015

4 minute read

4 minute read

By:

By: Current market situation

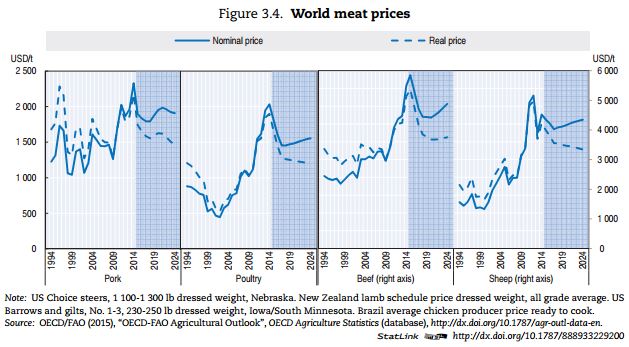

Meat prices reached record levels in 2014, driven mainly by an increasing beef price. At the same time, the Porcine Epidemic Diarrhoea virus (PEDv) in the United States and African swine fever in Europe, lowered pigmeat supply in 2014 pushing pigmeat prices upwards.

Sheepmeat prices also increased in 2014 following several years of flock reduction in New Zealand, induced by the conversion of sheep farms to more profitable dairy operations and accentuated by drought conditions whilst substitutability among the various meats ensured firm demand and strong poultry prices.

After several years of cow herd liquidation in major producing regions, the United States bovine sector in particular started a cattle herd rebuilding phase in 2014 that sent beef prices higher.

Although herd rebuilding is expected to support beef prices in the short term, the effects of PEDv are abating and hence the price of pork and poultry should follow lower feed grain prices.

Sheep meat prices remain high along with other meats, supported by higher import demand, particularly from China for mutton and the EU for lamb, combined with flock rebuilding in Australia.

Poultry sector main beneficiary of increased consumption

The Outlook for the meat market remains largely positive, with feed grain prices set to remain low for the projection period restoring profitability in a sector that had been operating in an environment of particularly high and volatile feed costs over most of the past decade.

Production is projected to expand, as a result of increased profitability, particularly in the pigmeat and poultry sectors, as well as in regions such as the Americas where feed grains are used intensively to produce meat.

However, this year’s Outlook is projecting weaker economic growth for both developed and developing countries, somewhat limiting consumption growth.

Nominal meat prices are expected to remain high throughout the outlook period, although below 2014 levels with the exception of beef which is expected to remain high for another two years, as herds are rebuilt in several parts of the world.

By 2024, prices for beef and pigmeat are projected to increase to around USD 4 900/t carcass weight equivalent (c.w.e.) and USD 1 900/t c.w.e. respectively, while world sheep meat and poultry prices are expected to rise to around USD 4 350/t c.w.e. and USD 1 550/t c.w.e. respectively.

In real terms meat prices are expected to trend down from their latest high levels, although they will remain higher than in the previous decade (Figure 3.4). Global meat production rose by almost 20 per cent over the last decade, led by growth in poultry and pigmeat.

Over the next decade, global meat production will expand at a slower rate, and in 2024 will be 17 per cent higher than the base period (2012-14).

Developing countries are projected to account for the vast majority of the total increase through a more intensive use of protein meal in feed rations in the region.

Poultry meat will capture more than half of the additional meat produced globally by 2024, compared to the base period.

In general production will also benefit from both improved meat-to-feed price margins as well as better feed conversion ratios in the next decade. Global annual meat consumption per capita is expected to reach 35.5 kg retail weight equivalent (r.w.e.) by 2024, an increase of 1.6 kg r.w.e. compared to the base period.

This additional consumption will consist mainly of poultry. Globally, per capita consumption of pig and bovine meat is expected to remain stable at levels comparable to the base period.

In absolute terms, consumption per capita of meat in developed countries is expected to remain more than double that in the developing countries (68 kg r.w.e. compared to 28 kg r.w.e. in 2024).

However, consumption growth in developed countries over the projection period is expected to remain slow relative to developing regions.

Rapid population growth and urbanisation within many developing regions remains a core driver of total consumption growth.

Fast-growing meat trade in Asia and Africa

Growth in meat trade is projected to decelerate compared to the past decade.

Globally almost 11 per cent of meat output will be traded. The most significant growth in import demand originates from Asia, which captures the greatest share of additional imports for all meat types. Africa is another fast growing meat importing region albeit from a lower base.

Although developed countries are still expected to account for slightly more than half of global meat exports by 2024, their share is steadily decreasing relative to the base period.

Brazil’s share of global exports is expected to remain stable at around 21 per cent, contributing to a quarter of the expected increase in global meat exports of the projection period.

Trade policies remain one of the main factors driving the outlook and dynamics in the world meat markets. The implementation of various bilateral trade agreements over the outlook period could diversify meat trade considerably.

The outbreak of PEDv in the United States has illustrated the extent to which disease outbreaks can affect both domestic and international markets. A reduction of almost 1.5 per cent in US supplies through 2014 contributed to higher pigmeat prices.

Globally, impacts of trade agreements or animal diseases vary significantly, however, depending on whether the region is an importer or exporter, as well as the magnitude of market share.

Further Reading

You can view the full OECD-FAO report by clicking here, and an expanded meat report is available here.