CME: US Chicken Production Growth Expected, but How Much?

US - This is the favourite time of year for grain analysts, taking long detours through corn and soybean fields, counting ears of corn and bean pods, examining how well they are filled, discussing drought impacts and, everyone’s favourite, issuing yield estimates, write Steve Meyer and Len Steiner. 25 August 2016

25 August 2016

2 minute read

2 minute read

By:

By: But even with all the arguing about final numbers, the broad consensus is that there will be mountains of corn looking for a home come fall and feed costs well below year ago levels.

Exports will help clean up some of that, although the increase may not be as big as some expect. There is a lot of cheap grain in the world and the headwinds of a strong US dollar have yet to subside.

Ethanol demand appears to have plateaued and is growing only as much as the increase in gasoline consumption can allow, i.e. not much.

Which leaves livestock and poultry production to absorb much of the increase in grain supplies. Now this can be done in two ways. You can have more animal units and you can feed those animal units to heavier weights so as to convert the feed into higher value protein.

We talk daily in this report about the hog and cattle markets but the big “animal unit” sitting in the corner is chicken.

The latest USDA data shows that while beef production next year is expected to increase by 838 million pounds and pork production will increase by 603 million pounds, chicken output growth at a modest 2.6 per cent growth rate represents a +1-billion-pound increase.

All three proteins next year will increase a combined 2.5 billion pounds (and +7.5 billion pounds since 2014). Shifts in chicken protein supplies will continue to be a significant factor for prices going forward.

True, in the short term the substitution effects of chicken vs. pork and especially beef are relatively small. Over time, however, the overabundance of chicken does tend to impact demand for other meats.

Have you tried chicken jerky? Actually was pretty good and I bet the margins on that package were excellent. But back to the chicken discussion.

At this point chicken producers are looking to balance the desire to expand given the low cost of feed with their ability to a) process all the chickens that they can grow; and b) not to overwhelm demand.

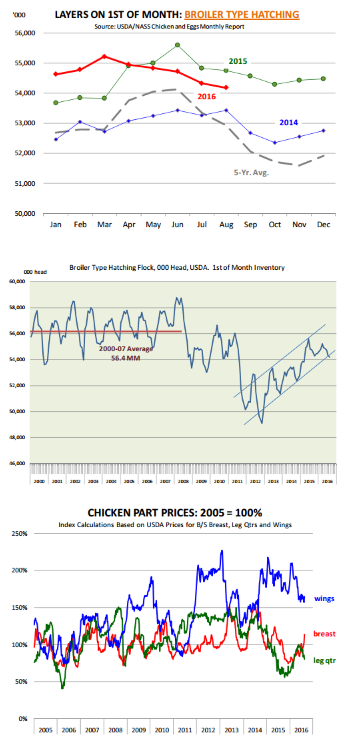

The latest data shows that producers are looking to reduce the size of the hatching flock. Some of this is seasonal and one can argue that last year producers maintained a larger flock as a hedge against a possible outbreak of Avian Influenza.

Disease outbreaks are always a risk but at this point the hatching flock is running about 1 per cent lower than a year ago but still about 8 per cent larger than during the 2012-13 supply contraction.

The smaller hatching flock so far has had no impact on the number of eggs set in incubators, which could reflect productivity gains. In the last six weeks’ egg sets have averaged 1 per cent above a year ago while chick placements are up 0.5 per cent.

More important for the chicken market in the short term, however, is the trend in weights. Weekly data is pointing to flat to even negative growth in broiler weights, which matches with what we are hearing in terms of pushback following quality concerns with extra-large chicken breasts.

For now, it appears to us that broiler supply growth remains on track and USDA is right to pencil in a less aggressive 2.5 per cent expansion rate for 2017.