CME: Mid-2011 Livestock & Poultry Supplies

US - Len Steiner and Steve Meyer take stock on US livestock and poultry supplies. 6 July 2011

6 July 2011

4 minute read

4 minute read

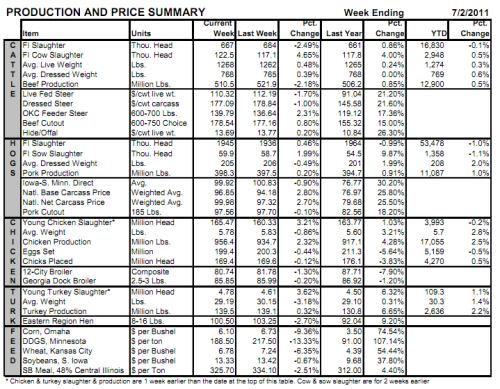

Based on daily data from USDA (shown in the Weekly Production and Price Summary figure), total beef, pork, chicken and turkey output amounted to 43.678 billion pounds, 2.4 per cent higher than one year ago.

That increase is driven primarily by growth in chicken (2.5 per cent) and turkey (2.2 per cent) output this year. Pork production is up one percent while beef production is 0.5 per cent higher through to second of July.

Note that these figures differ from the ones on the charts below because the charts represent weekly data and year-to-date (YTD) figures almost always differ slightly between daily and weekly data.

Beef production last week fell sharply from the prior week but remained slightly larger than the level of the same week last year.

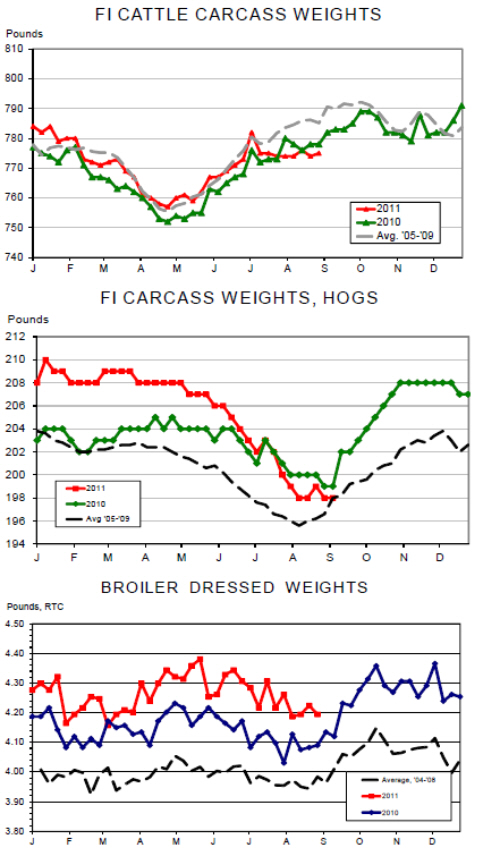

Total beef production was estimated to be 510.5 million pounds, down 2.2 per cent for the week but 0.9 per cent higher than in 2010. As can be seen in the top chart, year-on-year changes in beef output have spent portions of this year both above and below last year’s levels with the most recent weeks being higher.

Beef output over the past four weeks has exceeded last year’s level by 2.5 per cent. We expect higher output to persist into the autumn months given higher feedlot inventories. The key factor regarding how these output level change in late 2011 will be the level of placements in June and beyond. Recall that May placements were over 10 per cent lower than last year — finally reflecting the tight feeder cattle inventories in USDA’s first of January Cattle (inventory) report. The first of July inventory will be released on July 22.

Pork production remains very close to last year’s levels. Last week’s output of 398.3 million pounds was 0.2 per cent higher than the previous week and one per cent larger than the same week last year.

Over the past four weeks, US pork production was almost precisely the same as last year, differing by only 0.05 per cent.

Slaughter is expected (based on the June Hogs and Pigs Report) to exceed year-ago levels by about one per cent in the third quarter and be about even with last year in Q4 so the driver of any output change will be weights – which we expect to be lower and perhaps substantially so beginning in October.

Lower feed costs, though, may reduce the size of the weight declines.

Finally, chicken production exceeded year-ago levels by 4.3 per cent for the second straight week last week.

Recent reductions in egg sets and placements have not yet pulled slaughter levels down but we expect them to do so very soon – perhaps this week. The authors doubt, though, that average weights (+2.7 per cent YTD) will decline given the growth of the heavy bird sector and lower actual and expected feed costs.

Further Reading

| - | You can view the full report by clicking here. |