Meat Futures Focused on Asia Market Crisis

US - At this point, livestock futures are focused on the broader macro markets and threats of a brewing financial crisis in Asia, write analysts Steve Meyer and Len Steiner. 25 August 2015

25 August 2015

3 minute read

3 minute read

By:

By: For some, the recent events are reminiscent of 1997, which led to a broad recession in a number of Asian markets.

For livestock futures this is significant as Asia in recent years has emerged as a major buyer of meat products from North America, Oceania and South America.

In this context, cattle and hog markets are trying to price the impact of a dramatic slowdown in Asian demand, not just for US products but also products from other markets.

Already Russia, a major global meat protein buyer, has dramatically reduced its meat imports. A slowdown in Asia would add to that demand slack and pressure prices lower.

With this in mind, below are the highlights from the monthly USDA surveys.

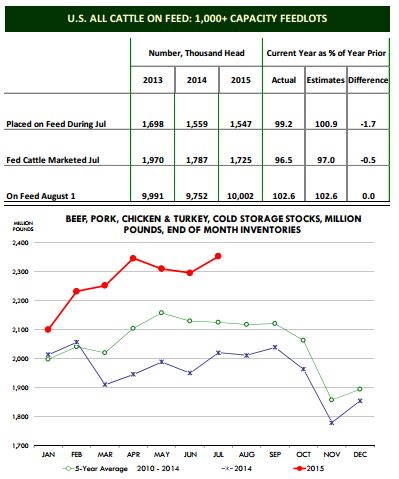

Cold Storage: Total supplies of beef, pork, chicken and turkey in cold storage at the end of July were 2.352 billion pounds, 16.5 per cent higher than a year ago and 10.7 per cent higher than the five year average (full details on page 3).

Inventories also increased 2.5 per cent from the previous month, something we saw last year but which normally does not happen.

The seasonal tendency is for inventories to be down in July. We view this as bearish for meat prices going into the fall.

Total beef inventories were 455.1 million pounds, 23.7 per cent higher than a year ago and 8.6 per cent higher than the five year average.

We think a big reason for the increase is due to larger beef imports during the first half of the year.

Beef inventories declined 4 per cent in July from the previous month. In the last five years July stocks have declined by an average of 2.2 per cent.

Pork inventories remain heavy and we see the big surge in ham stocks as bearish for the market going into the fall. The only caveat is if the large stocks represent pork that will go to export.

However, keep in mind that the biggest buyer of hams is Mexico and product does not need to be stored for long before it gets shipped.

We think the increase in ham stocks reflects large production during June and July that could not be fully absorbed. Given expectations of higher slaughter numbers in September and October, the large ham inventories remain bearish for ham prices this fall.

Belly inventories were 23.6 million pounds, 63.4 per cent lower than a year ago and 31.2 per cent lower than the five year average.

Total chicken inventories at 767.9 million pounds were 22.1 per cent higher than a year ago and 15.9 per cent higher than the five year average.

Overall chicken supplies remain burdensome, especially the large supply of chicken breast meat in storage.

Breast meat stocks at the end of July were 138.9 million pounds, 27.5 per cent higher than a year ago.

Cattle on Feed: Prior to the report analysts indicated that they expected placements to be up 0.9 per cent compared to a year ago but the USDA survey showed placements of cattle in feedlots with a capacity of +1000 cattle was down 0.8 per cent.

The difference is rather small in net cattle numbers. Marketings in July were down 3.5 per cent compared to estimates of a 3 per cent reduction.

The inventory of cattle on feed as of August 1 was up 2.6 per cent compared to a year ago the same as what analysts were projecting prior to the report.

Two factors are driving placements at this point:

a) very good pasture conditions that have provided a very strong forage base for cowcalf operators and allowed them to add weight to feeders outside of feedlots;

b) excellent cow-calf margins have provided plenty of incentive to retain more heifers in the herd.

Both of these factors should continue to limit cattle placements in the very near term and in July kept placements of US born feeder cattle under year ago levels.

Placements should increase seasonally later this fall but the latest data implies that slaughter numbers should be steady to only slightly higher later this year and in early 2016.