CoBank Quarterly: expected boost in fiscal spending lifts outlook

Vaccines bring optimism for economic recovery, but significant risks remain 18 January 2021

18 January 2021

1 minute read

1 minute read

By:

By: Shifts in the political landscape bring new legislative possibilities, including an increased probability of more COVID-19 financial aid and other fiscal spending, which are pushing up expectations for 2021 GDP growth.

According to the new Quarterly report from CoBank’s Knowledge Exchange, it will likely be summer before the economy really begins to gain steam, but the second half of the year should power the economy to annual growth of roughly 4.5%–5.5%.

“While the economic outlook has improved, significant risks still remain,” said Dan Kowalski, vice president of CoBank’s Knowledge Exchange division. “Key among those risks are the potential for more geopolitical crises, business solvency, a slower than expected receding of the pandemic and persistence in high rates of long-term unemployment.”

The steady climb in corn, soybean, and wheat prices during the fourth quarter of 2020 afforded growers and grain cooperatives the opportunity to capture significant margins. Since August, corn and soybean prices have risen more than 60% while wheat prices have gained more than 30%. The rally is a result of smaller-than-expected U.S. production; strong domestic demand for food, feed, and fuel; and continued large purchases by China, including its follow-through on actual grain shipments.

Farm supply retailers benefitted from the grain price rally and are poised for a favorable spring agronomy season, weather permitting. Armed with liquidity, growers took advantage of generally favorable weather to conduct post-harvest fall fertilizer applications and other field activities. It is likely that as farmers sought to mitigate tax liabilities by year-end, they increased prepayments to cooperatives, providing ag retailers with additional working capital.

The U.S. ethanol sector continued to recover during Q4, with average daily production reaching 14.7 billion gallons, equaling 90% of pre-COVID supply and demand levels. Operating margins retreated however to $0.11 per gallon, principally due to a dramatic 26% increase in corn input costs. Fuel ethanol’s production outlook could improve somewhat in 2021 if COVID-19 vaccine deployment fosters a return to workplaces. Although, a continued rise in corn prices will compress operating margins.

Profit margins for chicken producers during Q4 were generally below break-even, but average industry margins ended the quarter in a far better position than where they started, due to a 2% pullback in supply. What makes this margin improvement noteworthy is it occurred amid rising feed costs, but contraction in chicken supply helped prices for leg quarters, wings, and whole birds to climb through year-end.

© CoBank

© CoBank

The U.S. pork sector worked through the backlog of hogs over the summer and started the fourth quarter relatively current in most parts of the country. That along with the boost in trade expectations following the discovery of African Swine Fever (ASF) in Germany delivered the best spot producer margins of the year in October. These margins eroded through the quarter though as fears of capacity issues and higher feed costs began to take their toll, as did margins for pork packers.

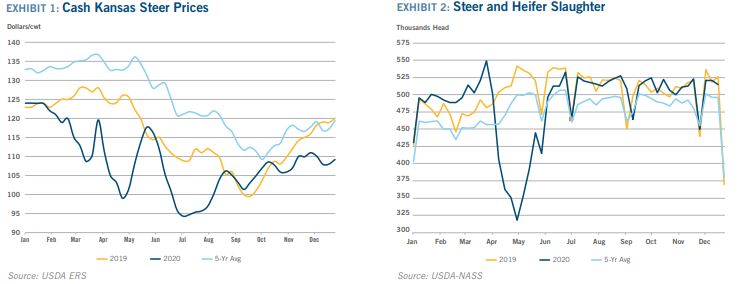

U.S. beef demand performed well during the fourth quarter, despite the challenging foodservice environment. The beef cutout made a strong rally in November as many consumers switched to beef for their holiday meals in light of smaller gatherings. With limited available industry capacity and a challenging labor environment, beef packers continue to benefit from strong margins and producers and feeders are increasingly focused on the feed market.

© CoBank

© CoBank

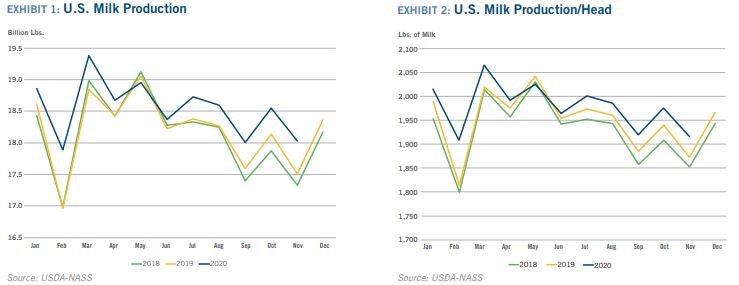

Milk and dairy products ended 2020 in ample supply despite the seasonal spike in holiday demand, which was down significantly compared to prior years. That could lead to even greater surplus supply issues for dairy producers and processors leading into the 2021 spring flush. USDA’s fifth round of food purchases under the Farmers to Families Food Box Program will be a needed short-term release valve for dairy products in the opening months of 2021.

Extreme tightness in South American rice supplies continues to support global rice prices heading into 2021, with the U.S. benefiting as the nearby rice exporter into the region. China remains the central figure behind the rally in U.S. cotton prices that ended the year up nearly 9%, while recoveries in crude oil and other commodities have helped cotton return to the highest level in two years.

© CoBank

© CoBank

The year-end collapse in natural gas prices is closing the door on a comeback for U.S. coal plants. To date, the COVID-19 fallout has not altered plans to retire coal-fired plants, with the next five years likely to witness a quickening pace of decommissioning. While the past decade saw 97 GWs of coal plant retirements, it’s quite possible that same capacity could be shuttered by mid-decade.

Read The Quarterly. Each CoBank Quarterly provides updates and an outlook for the Macro Economy and U.S. Agricultural Markets; Grains, Biofuels and Farm Supply; Animal Protein; Dairy; Specialty Crops; Other Crops and Rural Infrastructure Industries.